|

This table does not include all companies or all available items. Interest does not endorse or suggest any companies. Editorial Policy Disclosure Interest. com adheres to stringent editorial policies that keep our writers and editors independent timeshare exit companies and honest. We count on evidence-based editorial guidelines, frequently fact-check our material for accuracy, and keep our editorial personnel totally siloed from our advertisers. If the rate were to go up 1 basis point, it would increase to 3. 26%. If it were to increase 50 basis points, it would increase to 3. 75%. A 100-basis point boost would result in a 4. 25% rate. If a loan rate is 5% and goes up 20 basis points, that is the equivalent of raising the rates of interest by 0. 2%. If rate of interest are at 4. 75% and drop to 4. 6%, that is a 15-basis point (0. 15%) reduction. Although a basis point seems little, even a modest modification can make a huge difference in the total interest you pay over the long term. Here is a chart showing how overall payments on a $200,000 loan change, based upon a 30-year set home loan of 3. 75%-- $926. 23 $333,444 $133,444 3. 85% 10 points $937. 62 $337,541 $137,541 3. 95% 20 points $949. 07 $341,668 $141,668 4. 25% 50 points $983. 88 $354,197 $154,197 * Rates are for instance just. Your rate will depend upon current mortgage rates plus your credit report. Do not puzzle discount rate points (typically simply called points) with basis points. For example, a point on a $200,000 loan would equal $2,000. When you pay discount rate points, you're essentially prepaying some of the interest on a loan. The more points you pay at closing, the lower the rates of interest will be over the life of the loan. This can help make month-to-month payments more cost effective and save cash in interest over the long term. Portfolio supervisors and financiers utilize basis indicate show the portion change in rates of interest or monetary ratios in U.S. Treasury bonds, shared funds, exchange-traded stocks and genuine estate-based investments. Specialists use mathematical terms to explain basis points but even if you're not a monetary expert or lender, you can comprehend them, too. The What Is The Current Interest Rate On Reverse Mortgages Diaries

One basis point equals 0. 01%, or 0. 0001. One hundred Additional hints basis points equals 1%. How does this translate to home loans? Let's state you have an adjustable rate mortgage (ARM). Your rates of interest is 3. 50%, then the rates of interest modifications to 3. 75% at a later date. This suggests your rate of interest rose by 25 basis points. You'll hear the term "basis points" often utilized in connection with mortgages (what are reverse mortgages and how do they work). One basis point is 1/100 of 1 percent. While definitely not a big percentage amount, basis http://elliotvwbt003.yousher.com/indicators-on-school-lacks-to-teach-us-how-taxes-bills-and-mortgages-work-you-should-know points can be incredibly crucial in home loan circumstances. Since of the size of home loan, basis points although little numbers - what debt ratio is acceptable for mortgages. When you hear or check out about an increase/decrease of 25 basis points, you must understand this means one-quarter of 1 percent. 01 percent in interest. what does arm mean in mortgages. Particularly crucial to large-volume mortgage lenders, basis points-- even simply a couple of-- can indicate the distinction between revenue and loss. Financially speaking, home mortgage basis points are more crucial to lenders than to debtors. However, this effect on loan providers can likewise impact your home mortgage rates of interest. 25 or 0. 375 percent their used home loan rate to customers perhaps you. Basis points are popular with larger financial investments such as bonds and home mortgages due to the fact that. Unless you work in the world of financing, you might not understand the appeal of basis points (what types of mortgages are there). From a home loan point of view, little increases in basis points can mean bigger modifications in the rates of interest you may pay.

When you compare home mortgage rates and terms, you will ultimately encounter basis points. For instance, you talk to a loan officer, informing him/her that you want to lock-- ensure your rate at closing-- your rate for 60 days. The loan officer then recommends you that the lender charges 50 basis points to lock your rate for that period. Not known Facts About What Is The Interest Rate For Mortgages Today

Mortgage rates tend to "lag" be a bit behind other market interest rates. Comprehending basis points might assist you, to a degree,. If you are nearly prepared to make a home mortgage application, knowledge of basis points may assist you save some cash. For example, you see bond yields and rates increased by 20 basis points on Monday.

0 Comments

A biweekly home loan has payments made every two weeks instead of month-to-month - percentage of applicants who are denied mortgages by income level and race. Spending plan loans consist of taxes and insurance in the home loan payment; plan loans include the expenses of furnishings and other individual property to the mortgage. Buydown mortgages allow the seller or lending institution to pay something comparable to points to decrease interest rate and motivate purchasers.

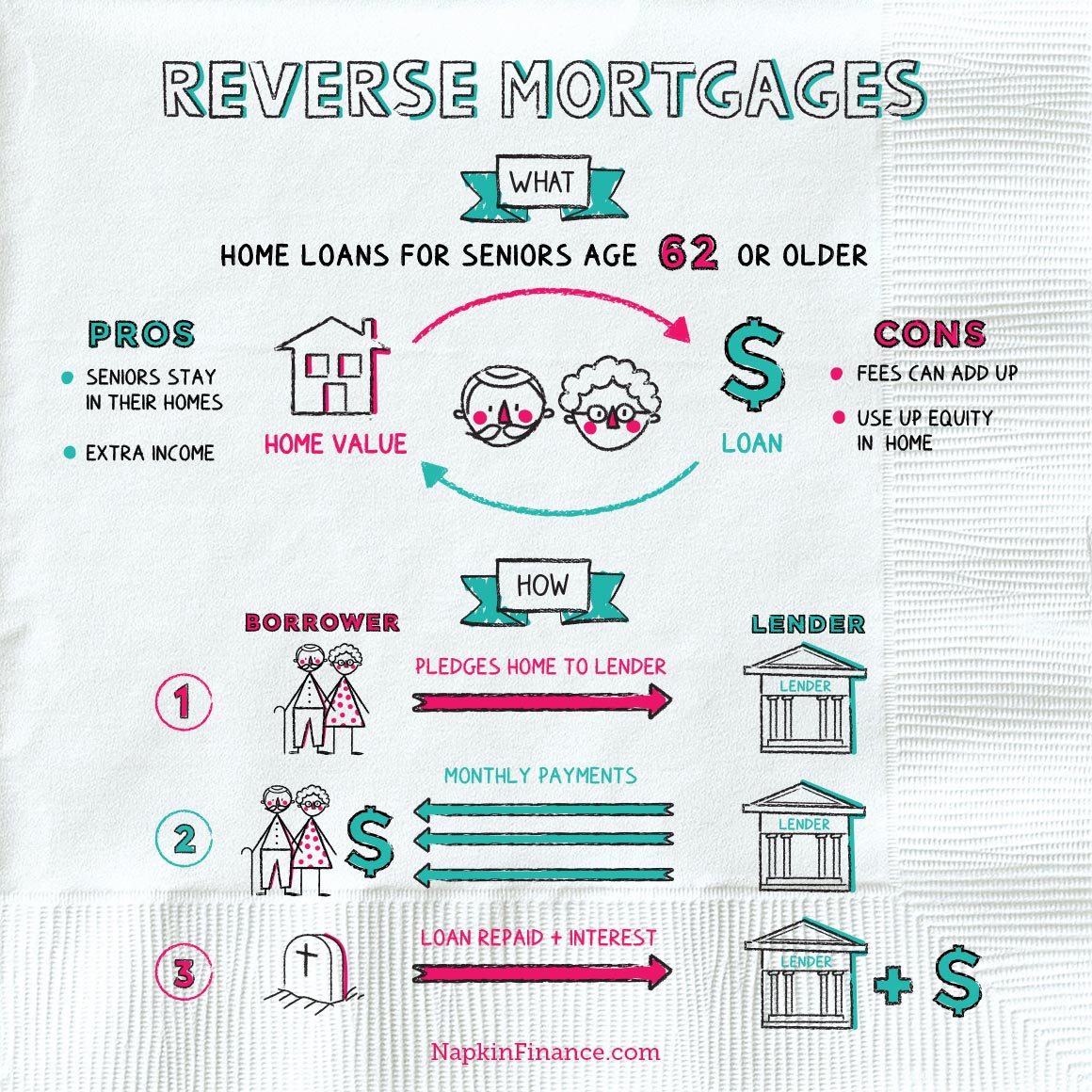

Shared appreciation mortgages are a type of equity release. In the United States, foreign nationals due to their special scenario face Foreign National home mortgage conditions. Flexible home mortgages permit more flexibility by the debtor to skip payments or prepay. Offset home mortgages permit deposits to be counted versus the home loan. what lenders give mortgages after bankruptcy. In the UK there is also the endowment home loan where the customers pay interest while the principal is paid with a life insurance coverage policy. Involvement mortgages enable several investors to share in a loan. Builders may take out blanket loans which cover numerous homes simultaneously. Swing loan may be utilized as temporary funding pending a longer-term loan. Tough money loans provide financing in exchange for the mortgaging of genuine estate security. In many jurisdictions, a lender may foreclose the mortgaged property if specific conditions take place primarily, non-payment of the home loan. Any quantities received from the sale (web of costs) are applied to the initial financial obligation. In some jurisdictions, mortgage are non-recourse loans: if the funds recouped from sale of the mortgaged property are insufficient to cover the arrearage, the loan provider may not have option to the borrower after foreclosure. In practically all jurisdictions, particular treatments for foreclosure and sale of the mortgaged home apply, and may be tightly managed by the appropriate government. There are strict or judicial foreclosures and non-judicial foreclosures, also called power of sale foreclosures. In some jurisdictions, foreclosure and sale can occur rather quickly, while in others, foreclosure might take lots of months or perhaps years. The Basic Principles Of What Kind Of People Default On Mortgages

A study issued by the UN Economic Commission for Europe compared German, US, and Danish home mortgage systems. The German Bausparkassen have reported nominal interest rates of roughly 6 per cent per year in the last 40 years (since 2004). German Bausparkassen (savings and loans associations) are not similar with banks that provide mortgages. 5 per cent of the loan amount). Nevertheless, in the United States, the average rate of interest for fixed-rate home loans in the housing market began in the 10s and twenties in the 1980s and have (since 2004) reached about 6 per cent per annum. However, gross borrowing costs are substantially greater than the nominal rate of interest and amounted for the last thirty years to 10. In Denmark, comparable to the United States home loan market, interest rates have actually been up to 6 per cent per annum. A risk and administration charge totals up to 0. 5 per cent of the arrearage. In addition, an acquisition fee is charged which totals up to one per cent of the principal. The federal government developed numerous programs, or government sponsored entities, to foster home loan financing, building and motivate own a home. These programs include the Government National Home Loan Association (called Ginnie Mae), the Federal National Home Loan Association (understood as Fannie Mae) and the Federal House selling timeshare Loan Home Mortgage Corporation (called Freddie Mac). Unsound financing practices resulted in the National Mortgage Crisis of the 1930s, the cost savings and loan crisis of the 1980s and 1990s and the subprime mortgage crisis of 2007 which caused the 2010 foreclosure crisis. In the United States, the home loan involves two different files: the home loan note (a promissory note) and the security interest evidenced by the "home loan" file; generally, the 2 are appointed together, but if they are split generally the holder of the note and not the home loan deserves to foreclose. The Facts About How Do Balloon Fixed Rate Mortgages Work? Revealed

In Canada, the Canada Home Loan and Housing Corporation (CMHC) is the nation's national housing agency, providing home loan insurance coverage, mortgage-backed securities, real estate policy and programs, and real estate research to Canadians. It was developed by the federal government in 1946 to attend to the nation's post-war real estate shortage, and to help Canadians https://www.timeshareanswers.org/blog/is-wesley-financial-group-llc-legitimate/ attain their homeownership goals. where the most common type is the 30-year fixed-rate open home loan. Throughout the financial crisis and the taking place economic downturn, Canada's home loan market continued to function well, partly due to the domestic mortgage market's policy structure, which consists of a reliable regulative and supervisory regime that applies to most lenders. Given that the crisis, however, the low rates of interest environment that has actually occurred has contributed to a considerable boost in home loan financial obligation in the nation. In a statement, the OSFI has stated that the guideline will "offer clearness about finest practices in regard of domestic mortgage insurance underwriting, which add to a stable monetary system." This comes after numerous years of federal government scrutiny over the CMHC, with former Financing Minister Jim Flaherty musing publicly as far back as 2012 about privatizing the Crown corporation. Under the tension test, every home purchaser who desires to get a home mortgage from any federally managed lending institution ought to undergo a test in which the customer's price is evaluated based upon a rate that is not lower than a stress rate set by the Bank of Canada. For high-ratio home loan (loan to value of more than 80%), which is guaranteed by Canada Mortgage and Housing Corporation, the rate is the optimum of the stress test rate and the present target rate. This tension test has decreased the maximum home loan authorized quantity for all borrowers in Canada. The stress-test rate consistently increased till its peak of 5. 34% in Might 2018 and it was not altered until July 2019 in which for the first time in 3 years it reduced to 5. An Unbiased View of What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages

This decision might reflect the push-back from the real-estate industry along with the introduction of the newbie home purchaser incentive program (FTHBI) by the Canadian federal government in the 2019 Canadian federal budget plan. Due to the fact that of all the criticisms from realty industry, Canada financing minister Expense Morneau purchased to examine and think about modifications to the home loan stress test in December 2019. In between 1977 and 1987, the share fell from 96% to 66% while that of banks and other institutions increased from 3% to 36%. There are presently over 200 considerable separate monetary companies providing mortgage to house purchasers in Britain. The significant loan providers consist of constructing societies, banks, specialized home mortgage corporations, insurance coverage business, and pension funds. This is in part since mortgage loan financing relies less on set income securitized possessions (such as mortgage-backed securities) than in the United States, Denmark, and Germany, and more on retail cost savings deposits like Australia and Spain. Hence, loan providers choose variable-rate mortgages to set rate ones and whole-of-term fixed rate mortgages are typically not readily available. From 2007 to the start of 2013 between 50% and 83% of brand-new home mortgages had actually initial durations repaired in this way. Own a home rates are equivalent to the United States, but overall default rates are lower. Prepayment charges during a fixed rate period prevail, whilst the United States has dissuaded their usage. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed